Picking up a prescription and finding out your insurance will not cover it is one of the more frustrating moments in dealing with health care. You assumed the coverage was there, the pharmacist gives you a number that does not make sense, and suddenly you are making a decision about medication you need while standing at a pharmacy counter.

This happens far more often than it should, and in most cases it is preventable. Insurance plans cover prescriptions in specific ways that are not always explained clearly at enrollment time. Understanding how drug coverage actually works, what your plan requires before it will pay, and how to push back when coverage is denied gives you real control over what you spend on medications each month.

This article covers the structure of prescription drug coverage, the steps that get more medications covered, and what to do when your insurer says no.

How Insurance Plans Decide What They Will and Will Not Cover

Every health insurance plan that includes prescription drug coverage maintains a formulary. That is the official list of drugs the plan covers and the cost-sharing terms attached to each one. Formularies are divided into tiers, and the tier your medication lands on determines how much you pay out of your own pocket.

Tier 1 typically includes generic drugs and carries the lowest copay, often just a few dollars per fill. Tier 2 covers preferred brand-name drugs at a moderate cost. Tier 3 covers non-preferred brand-name drugs at a higher cost. Higher tiers exist for specialty medications, biologics, and drugs that require special handling, and those costs can be substantial even with insurance. The tier assignment is made by the insurer, not by your doctor, and it can change from year to year when plans update their formularies during open enrollment.

Before filling any new prescription, checking whether the drug is on your plan’s formulary and which tier it falls under takes about two minutes through your insurer’s website or member portal. Most plans have a searchable drug list that shows exactly what you will owe per fill under your current coverage. Doing this before you get to the pharmacy means no surprises and gives you time to ask your doctor about alternatives if the cost is higher than expected.

Generic drugs are almost always cheaper than brand-name versions and are therapeutically equivalent to the original in the vast majority of cases. If your doctor prescribes a brand-name drug and a generic version exists, asking specifically for the generic at the time of the appointment is the single fastest way to reduce your prescription cost. Some doctors write brand-name prescriptions out of habit and will switch without hesitation if you ask.

Steps to Take When Your Insurance Will Not Pay

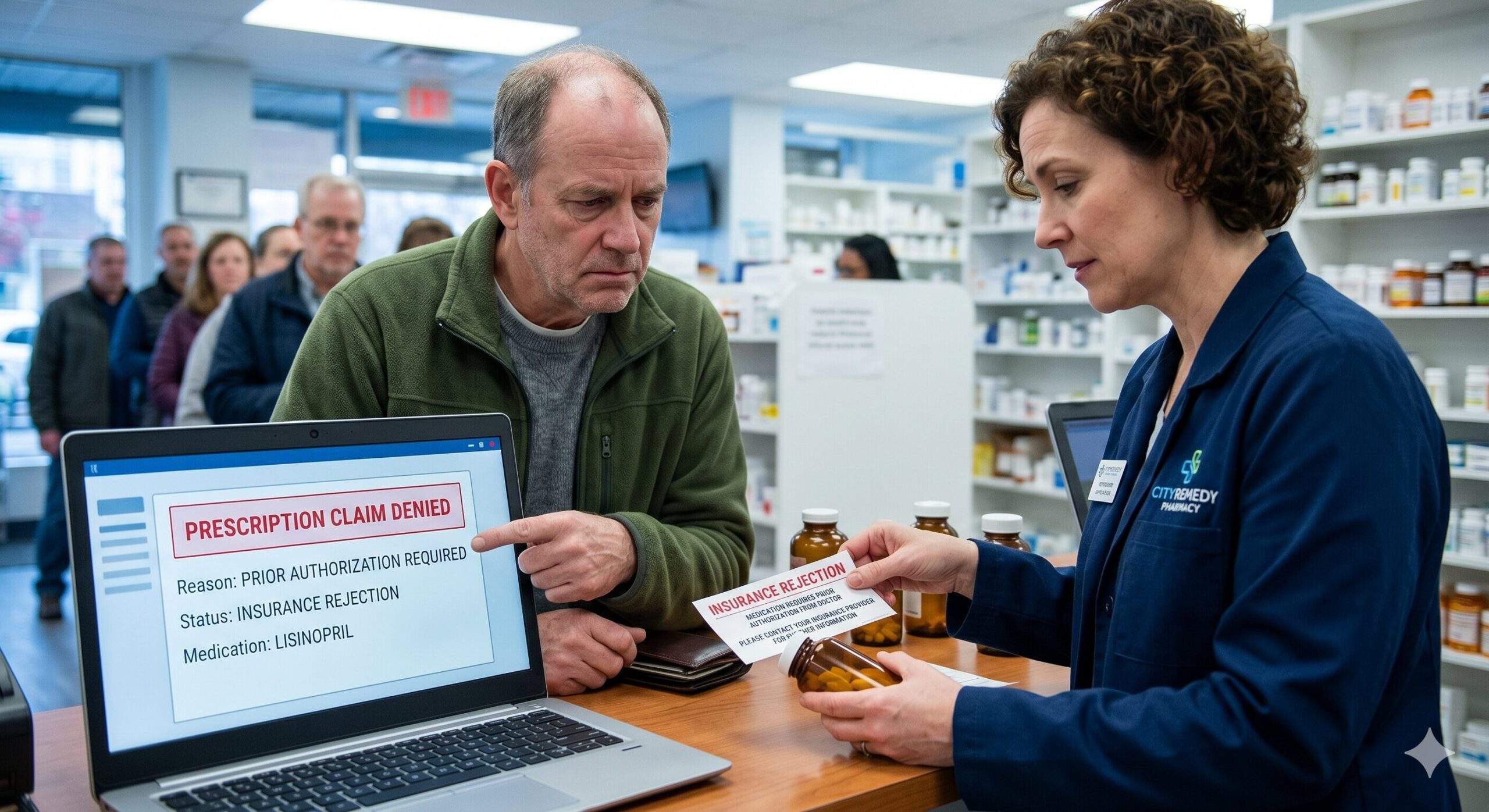

A coverage denial at the pharmacy is not always the final word. Insurance plans have built-in processes for challenging formulary decisions, and using them produces results more often than people expect.

- The first step is to ask the pharmacist to run a coverage check and confirm exactly why the claim was rejected. Common reasons include the drug not being on the formulary, the plan requiring a prior authorization before it will cover the medication, a quantity limit being exceeded, or a step therapy requirement not being met. Each of these has a different solution, and knowing which one applies tells you what to do next.

- Prior authorization is one of the most common barriers. It means your insurer wants your doctor to submit clinical documentation showing that the prescribed medication is medically necessary before they will approve coverage. It sounds like a bureaucratic obstacle, and it often is, but the process works. Call your doctor’s office, explain that the pharmacy flagged a prior authorization requirement, and ask them to submit the request. Most practices have staff who handle prior authorizations regularly and know exactly what the insurer needs to see. Approval can sometimes come through within 24 to 48 hours, though more complex cases take longer.

- Step therapy requirements are another common reason coverage is denied. This policy requires you to try a less expensive medication first before the plan will approve coverage for a more expensive one. If your doctor prescribed a newer or higher-tier drug, your insurer may require documentation showing that a first-line option was tried and either failed or caused problems. Your doctor can submit a step therapy exception if there is a clinical reason the standard first-line treatment is not appropriate for you specifically.

- If authorization is denied after your doctor submits the request, you have the right to appeal. Insurers are required to have an internal appeals process, and after that, an external review by an independent organization is available if the internal appeal fails. The appeals process takes time, but it is worth pursuing for any medication that is expensive or critical to your health. Your insurer’s member services line can explain the specific steps for your plan.

- Manufacturer patient assistance programs are worth checking in parallel. Many pharmaceutical companies offer free or reduced-cost medication directly to patients who cannot afford the out-of-pocket cost, regardless of insurance status. NeedyMeds.org and RxAssist.org both maintain searchable databases of these programs organized by drug name.

Using Your Plan Structure to Keep Prescription Costs Low

Beyond handling specific denials, understanding how your plan is structured lets you make smarter decisions about prescriptions throughout the year rather than reacting to problems as they come up.

The relationship between your prescribing doctor and your insurance network matters more than most patients realize. A doctor who is in-network and familiar with your plan’s formulary is far more likely to prescribe medications covered at your plan’s lowest cost tier from the start. When a doctor recommends a medication, asking whether it is covered by your plan and whether a preferred alternative exists on the formulary is a reasonable and straightforward question that most physicians are happy to answer.

Choosing a primary care doctor who coordinates your overall care well is part of this. A doctor who knows your full medication list, understands your insurer’s formulary preferences, and actively considers cost when writing prescriptions saves you money consistently over time. That kind of relationship starts with selecting the right doctor network during enrollment, because an in-network physician has far more leverage with your insurer on prior authorizations and appeals than an out-of-network provider does.

Mail-order pharmacies are another underused option for reducing costs on maintenance medications you take regularly. Most insurance plans offer a lower per-dose cost for a 90-day supply filled through a mail-order pharmacy compared to a monthly 30-day fill at a retail location. If you take a daily medication for a chronic condition, switching to mail order for that prescription alone can produce meaningful savings over a full year without changing anything about the medication itself.

Pharmacy discount programs like GoodRx, Cost Plus Drugs, and similar services operate entirely outside of insurance and sometimes produce a lower price than your insurance copay on certain generic medications. It is worth checking the cash price through one of these programs before assuming your insurance is always the cheapest option. You cannot use both insurance and a discount card on the same prescription, but for lower-tier generics the cash price through a discount program occasionally beats the insured price by a meaningful margin.

Frequently Asked Questions

What is a formulary and why does the tier matter?

A formulary is the official list of drugs your plan covers, divided into tiers that determine your copay. Tier 1 (generics) is typically a few dollars per fill, Tier 2 (preferred brand) sits in the middle, and Tier 3 (non-preferred brand) plus specialty tiers carry the highest cost. Check your insurer’s online drug list before filling any new prescription so you know the tier and copay in advance.

What should I do first when the pharmacy says a drug is not covered?

Ask the pharmacist to run a coverage check and confirm the exact rejection reason. It will be one of four things: not on the formulary, prior authorization required, quantity limit exceeded, or step therapy not met. Each has a different fix, so identifying which one applies tells you whether to call your doctor for documentation or request a formulary exception.

How does prior authorization work and how long does it take?

Prior authorization means your insurer wants clinical documentation from your doctor proving the medication is medically necessary before they pay. Call your doctor’s office, tell them the pharmacy flagged a PA requirement, and ask them to submit the request. Most practices handle these regularly and approval typically comes through in 24 to 48 hours, though complex cases run longer.

When does it make sense to skip insurance and use GoodRx or Cost Plus Drugs?

For lower-tier generics, cash prices through GoodRx, Cost Plus Drugs, and similar discount programs sometimes beat your insurance copay. Check the cash price before filling. You cannot stack a discount card with insurance on the same prescription, so it is one or the other, but on generics the discount route occasionally wins by a meaningful margin.

How can I save on a daily medication I take long-term?

Switch chronic medications to a 90-day mail-order fill. Most plans charge a lower per-dose cost for mail order than for monthly 30-day retail refills, so a single switch on one maintenance drug produces year-over-year savings without changing the medication itself. Confirm the mail-order pharmacy with your plan, then ask your doctor to write the prescription for a 90-day supply with refills.

Leave a Reply